Essential Guide to Workers’ Compensation Insurance for Small Businesses

Table of Contents

-

What Is Workers’ Compensation Insurance?

-

Why Small Businesses Need Workers' Comp Coverage

-

Common Myths and Misconceptions

-

How Much Does Workers’ Compensation Insurance Cost?

-

Workers’ Compensation Laws and Regulations

-

Filing a Claim: What to Expect

-

Tips for Choosing the Right Policy

-

Future Trends in Workers’ Compensation Insurance

What Is Workers’ Compensation Insurance?

Workers’ compensation insurance protects employees and businesses when an accident or illness is directly linked to work. It is much more than a mandatory checkbox—it’s an essential shield that ensures employees can access financial support for medical bills, rehabilitation, and some lost wages during recovery. As rules and requirements differ from state to state, it is crucial for business owners to carefully study specific solutions, such as policies for businesses in California, which can have unique terms, eligibility factors, and compliance obligations for local companies.

Workplace accidents happen even when the risk seems low. Statistics from the Insurance Journal show that millions of nonfatal injury and illness cases are reported among private-sector workers each year. This reality demonstrates just how universally necessary workers’ comp really is. Medical care for a seemingly minor injury can quickly add up, and covering these costs out-of-pocket may be overwhelming for a business and devastating for an individual employee. Workers’ comp insurance addresses these challenges, filling a crucial gap between day-to-day operations and unforeseen emergencies.

Why Small Businesses Need Workers' Comp Coverage

For many small business owners, a single injured employee can strain budgets or threaten business continuity. Workplace accidents—whether slips, repetitive strain injuries, or accidents with tools or vehicles—can happen anywhere, to anyone. Even when state law does not explicitly require coverage for all situations, workers’ compensation remains an intelligent and compassionate choice. The risk of costly lawsuits over medical expenses or lost wages can be drastically reduced with the proper coverage. Moreover, failing to maintain required insurance may result in severe penalties and, in some states, the loss of business licenses.

Many entrepreneurs bemoan the added cost and paperwork at first, but offering coverage boosts employee confidence and loyalty. Knowing that their employer values their health creates a positive work culture and reassurance among staff. Workers' compensation in food service, retail, construction, or professional offices sends the message that every team member’s well-being matters, which can translate into improved morale and long-term retention.

Common Myths and Misconceptions

-

“We’re a small, low-risk company.” – It’s a common misconception that only high-risk facilities need workers’ comp. In reality, injuries can happen in any workplace—from coffee spills causing slips in a café to carpal tunnel from computer work in an office environment. Regardless of company size or industry, every employer can benefit from a well-structured policy.

-

“It only kicks in for serious accidents.” – Many assume claims are only relevant for catastrophic injuries. However, workers’ comp typically covers a spectrum of incidents, including repetitive stress disorders, minor cuts, strains, and even illnesses developed from workplace exposures.

-

“Freelancers and contractors are always excluded.” – The boundaries between contractor and employee status can be complicated. While some states don’t require coverage for all independent contractors, the lines can blur with the specifics of each contract and job, leading to cases where freelance workers are eligible for benefits if misclassification occurs.

Misinformation often leads to insufficient protection or unexpected legal trouble. Every business should embrace a proactive approach that involves staying updated on facts with a reliable legal or insurance advisor and periodically reviewing policies as state definitions and rules evolve.

How Much Does Workers’ Compensation Insurance Cost?

The coverage price is highly individualized and is influenced by factors such as your industry, employee roles, claims history, payroll size, and even your physical business location. Sectors like roofing, transportation, and manufacturing historically face more frequent or severe injuries, thus face steeper premiums. By contrast, administrative or digital services companies may benefit from significantly lower rates. According to the Bureau of Labor Statistics, businesses in high-risk fields pay considerably more per employee than those in lower-risk environments.

A clean safety record and ongoing workplace training can decrease premiums over time. Some insurers offer credits or discounts for businesses that implement formal health and safety programs. Proactive claims management, returning injured employees to work in modified roles, and regular policy reviews are all strategies that not only contain costs but encourage a healthier, safer workplace for everyone involved.

Workers’ Compensation Laws and Regulations

Workers’ compensation requirements are not consistent across state lines. Some states require every employer to carry coverage, even with just one staff member, while others set the threshold at three, four, or five workers. The potential for confusion is high, especially for expanding companies and those with remote or seasonal workers across multiple states. Noncompliance penalties can include hefty fines, back payments, stopped work orders, and personal liability for business owners.

It’s wise to regularly review state-by-state workers’ compensation requirements to ensure you remain compliant as your business grows or diversifies. Consult with a professional who understands the unique requirements for your operations, and keep meticulous records to simplify audits and claims handling in the future.

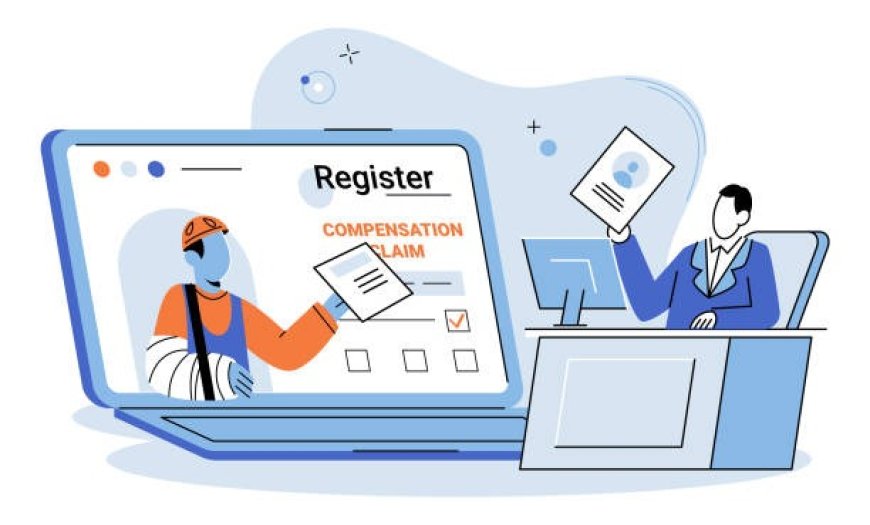

Filing a Claim: What to Expect

-

Employee reporting: Any work-related injury or illness should be reported to management immediately, even if it initially seems insignificant. Delayed reporting can lead to complications when a minor injury requires extended or costly care.

-

Documentation: The employer must supply claim paperwork, record details of the incident, and submit information to the insurer. Accurate documentation, including witness statements or photos, can speed up the process.

-

Claims process: The insurance carrier examines evidence, may interview staff, and coordinates medical assessments. Prompt communication with the provider helps ensure employees get care faster and mitigates administrative delays.

-

Receiving benefits: Once a claim is approved, the injured employee is entitled to wage replacement (often a portion of lost pay) and paid or reimbursed medical expenses as detailed in the policy.

Open dialogue with employees and preparation, including clear signage and processes, ensure that claims go smoothly, protecting both business interests and worker welfare.

Tips for Choosing the Right Policy

-

Explore several insurance providers to get a genuine sense of the market. Price is crucial, as is the service reputation and responsiveness when handling claims.

-

Scrutinize policy exclusions and waiting periods—know exactly what’s covered, what’s excluded, and when benefits will begin after an incident.

-

Partner with an agent or broker who understands your sector. The nuances of workers’ comp can vary dramatically depending on whether you run a warehouse, a creative agency, or a café.

-

Commit to a regular review schedule. Annual or biannual reviews ensure that significant changes in your business—new hires, roles, or locations—are accurately reflected in your policy.

The right policy is not always the cheapest one. It’s about finding a good match for your risk profile, employee mix, and business goals to provide sustainable, long-term protection for everyone under your roof.

Future Trends in Workers’ Compensation Insurance

The landscape surrounding workers’ compensation insurance is constantly shifting. Digital claim submissions, telemedicine for workplace injuries, and rapid online processing are becoming standard features, allowing businesses and employees to save time and avoid unnecessary delays. Additionally, the conversation is expanding to include mental health challenges related to the workplace, with particular insurers piloting new programs that offer mental health resources or coverage for work-related stress conditions.

Insurers and regulators regularly update rules and coverage options as industries change, especially with the rise of remote work, gig economy positions, and non-traditional employment models. Staying informed and adaptable allows small businesses to proactively address risks, navigate new regulations, and provide a supportive, competitive environment for current and prospective employees.